Table Of Content

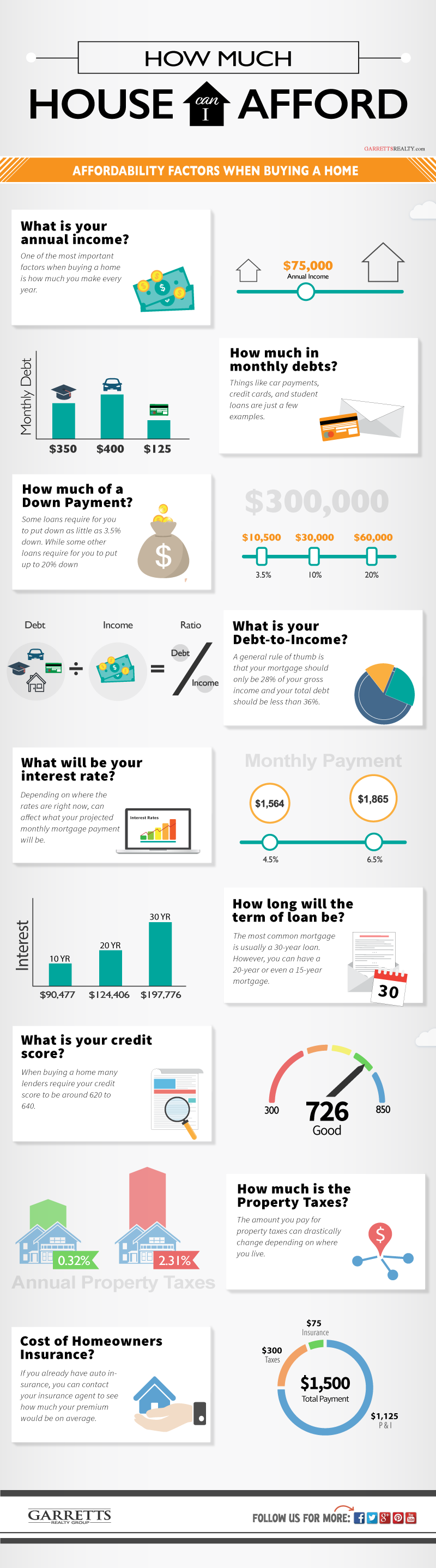

You’ll also need to factor in how mortgage insurance premiums — required on all FHA loans — will impact your payments. A house is one of the biggest purchases you can make, so figuring out how much you can afford is a key step in the home-buying process. To figure out how much home you can afford with our calculator, enter your gross annual income and total monthly debts, choose a down payment amount and select a loan term.

How to use our mortgage affordability calculator

Let’s go over some of the inputs to our home affordability calculator, plus some extra factors you’ll want to consider. Check today’s rates to see what you might qualify for and how much house you can truly afford. Also, since the equation does not account for down payments, it can be used when you’re refinancing your home. Similarly, if your home’s value rises, your equity percentage will increase by an amount greater than what you’ve paid in principal. You can ask for a mortgage pre-approval or a prequalification to see your loan options and “real” budget based on your personal finances.

Debt-to-Income Ratio

To find a financial advisor who serves your area, try SmartAsset's free online matching tool. Our partners cannot pay us to guarantee favorable reviews of their products or services. Input these numbers into our Home Affordability Calculator to get a clear idea of your homebuying budget. Bankrate follows a stricteditorial policy, so you can trust that our content is honest and accurate. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions. The content created by our editorial staff is objective, factual, and not influenced by our advertisers.

Documents needed for mortgage application

In San Francisco County, wages grew 6.6 percent while housing prices increased 5.3 percent, to $96,361. Programs, rates, terms and conditions are subject to change without notice. Understanding the difference — and then using a home affordability calculator to crunch some numbers — will help you decide how much house you can really afford. While your lender is willing to loan you a substantial amount of money, that doesn’t mean you have to borrow the entire amount if it would put you under significant financial strain. Both the upfront fee and the annual fee will detract from how much home you can afford.

Do you have enough savings that a down payment won’t drain your bank account to zero? If your personal finances are in excellent condition, a lender will likely be able to give you the best deal possible on your interest rate. For example, let’s say that you could technically afford to spend $4,000 each month on a mortgage payment. If you only have $500 remaining after covering your other expenses, you’re likely stretching yourself too thin. Remember that there are other major financial goals to consider, too, and you want to live within your means. Just because a lender offers you a preapproval for a large amount of money, that doesn’t mean you should spend that much for your home.

VA Loans

Mortgage Calculator: Estimate Your Monthly Payments - Business Insider

Mortgage Calculator: Estimate Your Monthly Payments.

Posted: Mon, 01 Apr 2024 07:00:00 GMT [source]

20 minutes southeast of downtown Los Angeles is the suburb of Pico Rivera. With a population of close to 62,000, you’ll be in a smaller town while being able to explore Los Angeles in your free time. If you find yourself moving to our fifth most affordable suburb, make sure to visit Pico Rivera Sports Arena for their yearly Colombian festival, El Festival Colombiano. PMI costs are determined using a generic pricing sheet by Enact Mortgage Insurance. The industry often uses pricing more specific to a borrower’s situation, so your PMI costs could be higher or lower than shown here. In December, prices jumped 4.4 percent year-over-year, compared to the average annual wage increase of 2.7 percent, to $64,197.

PMI is usually .05-1% of the cost of the home loan but may vary depending on credit score. Federal Housing Agency mortgages are available to homebuyers with credit scores of 500 or more and can help you get into a home with less money down. If your credit score is below 580, you'll need to put down 10 percent of the purchase price. If your score is 580 or higher, you could put down as little as 3.5 percent. In most areas in 2023, an FHA loan cannot exceed $472,030 for a single-family home. In higher-priced areas, the number can go as high as $1,089,300.

Likely rate: 7.422% Edit rate

The best way to determine how much mortgage you can qualify for is to start the mortgage application process. Look at your full financial picture after you’ve tracked your income and expenses for a few months. For example, if you realize you have $3,000 left over at the end of each month, decide how much of that could be allocated toward a mortgage. Mortgage term refers to the length of time you have to pay back the amount you’ve borrowed.

Fun-Filled Things to Do in Lake Elsinore, CA if You’re New to the City

For example, a 6.5% rate on a $300,000, 30-year loan means a payment of $1,896 per month and more than $382,633 in interest over the loan term. Rates, payments, and all information displayed are for informational purposes only and are subject to change without notice. Mortgage rates and terms you may qualify for depend on your individual financial circumstances. That’s a big deal, because mortgages backed by the Department of Veterans Affairs typically don’t require a down payment.

Key factors in calculating affordability are 1) your monthly income; 2) cash reserves to cover your down payment and closing costs; 3) your monthly expenses; 4) your credit profile. → The 28 is a recommended DTI ratio for your monthly mortgage payment compared to your gross monthly income. So the higher your rate, the less house you’ll be able to afford. Lenders divide your total monthly debt payments by your income to determine whether or not you can afford another loan. If you carry a lot of debt, lenders may require a higher credit score or extra mortgage reserves to cover a few month’s worth of mortgage payments.

Mortgage interest is the cost you pay your lender each year to borrow their money, expressed as a percentage rate. The calculator auto-populates the current average interest rate. Working towards achieving one or more of these will increase a household's success rate in qualifying for the purchase of a home in accordance with lenders' standards of qualifications. If these prove to be difficult, home-buyers can maybe consider less expensive homes. If not, there are various housing assistance programs at the local level, though these are geared more towards low-income households.

Bellflower has about 79,000 residents and is a great suburb to consider moving to, offering you access to many Southern California staples. From the Hollywood Sports Paintball & Airsoft Park to The Los Angeles County Fire Museum, you’ll be close to what makes Bellflower unique. Check out our guide to finding open houses in your area, plus tips on how to prepare for them. There are several steps in the house-shopping process, from getting initial mortgage approval to viewing a house in person.

And you’re not alone—78% of homebuyers had to finance their home purchase in 2022, according to the National Association of Realtors. Before you get a mortgage, it’s critical to know how much home you can afford, especially as homes become more expensive. Using a mortgage calculator is a good way to get an idea of how much house you can afford. But only a lender can verify your mortgage eligibility and your home buying budget.

How much you ultimately will be approved for depends on several factors specific to your situation. Multiple mortgage brokers said they find lenders will generally approve you for conforming loans if your debt-to-income ratio doesn’t exceed 45%. Only 25 percent could afford the purchase, the association found, up from 22 percent at this time last year. The association credits the uptick to lower borrowing costs and higher incomes.

This means they can stay the same or change over the life of the loan. Your rate can be higher or lower depending on your credit score, down payment and other factors. Although your DTI and housing expense ratios are important factors in mortgage qualification, other variables impact your monthly mortgage payment and how much you can afford. On the flip side, if you have a price in mind, you can use a mortgage calculator to see how much cash you’ll need for a down payment and closing costs. There are no set rules regarding how much of your income should cover a mortgage payment. However, lenders will look at how much of your income is going to other outstanding debts before approving another loan.

Next up are several factors that can help you figure out the right price range before you hit the pavement looking for a new home. Read on to calculate how much house you can afford and learn what this means for whether you should buy a house. Budget 1% to 4% of your home’s value each year for home maintenance.

No comments:

Post a Comment